This website uses cookies. We use cookies to personalise content and ads, to provide social media

features and to analyse our traffic. We also share information about your use of our site with our

social media, advertising and analytics partners who may combine it with other information that

you’ve provided to them or that they’ve collected from your use of their services. You consent to

our cookies if you continue to use our website.

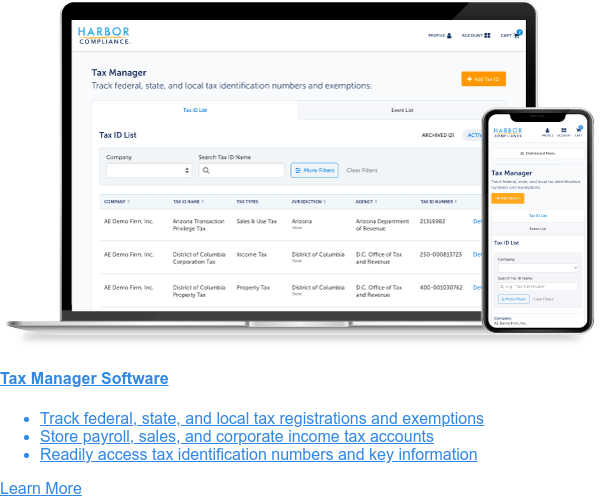

Applying for state tax IDs & tax exemption certificates

Registering for corporate income and privilege tax accounts is a requirement for many businesses.

Nonprofits that are tax exempt on the federal level are often eligible to apply for exemption from these

taxes. State tax authorities penalize companies that do not comply with the laws to register for and pay

corporate income tax. This guide summarizes the key concepts involved in obtaining tax identification

(ID) numbers, applying for exemption certificates, and maintaining corporate income tax compliance.

Introduction to Corporate Income & Privilege Tax

Corporate income tax is a tax on the net income of corporations. In most cases, only corporations are

subject to this tax.

Privilege taxes are imposed on businesses for the right to conduct business in a given state. Privilege

taxes are usually based on the gross receipts or net worth of a business, but some are levied as a flat

fee. States often use terms like franchise tax, business entity tax, or business and occupation tax to

refer to their local privilege tax. Some states have privilege taxes that apply to very specific groups

of businesses, such as banks or other financial institutions, but this guide does not cover those taxes.

Exemptions from corporate income and privilege tax are frequently available to nonprofits that are

federally exempt from income tax. While in some jurisdictions your organization must expressly apply for

an exemption, in others your organization is automatically exempt upon receiving federal exemption.

Nexus is the technical term for when an entity is legally subject to certain taxes in a given state. The

definition varies by governing authority, but in general it is a good idea to review corporate income

and privilege tax nexus when:

You set up your business.

You open a physical location in a new state.

You hire an employee or contractor in a new state.

You partner with an affiliate in a new state.

You store products, distribute products, or work with a drop-shipper in a new state.

Your company changes its business structure (e.g. LLC to corporation)

Where Corporate Income & Privilege Tax is Levied

All states except for South Dakota and Wyoming subject businesses to a combination of corporate income

and privilege taxes. Forty four states and the District of Columbia currently impose corporate income

taxes on corporations, while seventeen states levy broadly applicable privilege taxes.

Not all corporate taxes are levied or administered by the state. Some cities and counties levy general

business privilege taxes on entities located within their jurisdiction. This requirement is most

commonly held in heavily populated cities or counties.

Registering to File Corporate Income and Privilege Taxes

In each jurisdiction where registration is required, the entity applies for a tax ID, pays estimated

income taxes per the required schedule, and files a corporate tax return at the end of the year.

Although almost every state has a corporate income or privilege tax, relatively few states require

registration prior to filing a return.

Currently only twenty states require registration before a business files its first income tax return.

After registration, entities are issued a department of revenue identification number. Ohio and

Pennsylvania, however, issue an ID that is specific to the corporate income tax account. States that do

not require registration simply use the federally issued employer identification number to track

businesses.

Getting Corporate Income and Privilege Tax Exemption Certificates

In many states, nonprofits are automatically exempt from corporate income and privilege taxes after

receiving their IRS determination letter. Seventeen states and the District of Columbia, however,

require nonprofits to submit an application or supporting documentation before an exemption is granted.

Nonprofits should not assume they are exempt from paying corporate income and privilege taxes. The chart

below outlines each state-level process for obtaining exemption.

File an initial business privilege tax return within 2.5 months after the date of incorporation or qualification to register for the privilege tax.

Alaska

Alaska

Corporation

Not required

There is no need to register before filing corporation income tax.

More information: Alaska Department of Revenue

LLC

Not required

LLCs will typically file partnership income tax, but this depends of how the IRS classifies them. There is no need to register before filing partnership income tax.

More information: Alaska Department of Revenue

Arizona

Arizona

Corporation

Not required

There is no separate registration for corporate income tax.

More information: Arizona Department of Revenue

LLC

Not required

LLCs will typically file partnership income tax, but this depends of how the IRS classifies them. There is no separate registration for partnership tax.

More information: Arizona Department of Revenue

Arkansas

Arkansas

Corporation

Not required

There is no need to register before filing a corporation income tax return. The secretary of state administered franchise tax also does not require registration.

More information: Arkansas Department of Finance and Administration

LLC

Not required

Most LLCs do not file Corporate Income Tax returns. The secretary of state administered franchise tax also does not require registration.

More information: Arkansas Department of Finance and Administration

California

California

Corporation

Not required

There is no need to register with the Franchise Tax Board.

More information: California Franchise Tax Board

LLC

Not required

More information: California Franchise Tax Board

Colorado

Colorado

Corporation

Not required

There is no need to register for a Business Income tax account.

More information: Colorado Department of Revenue

LLC

Not required

Most LLCs will file form 106, Business Income Tax Return for Pass-Through Entities, to confirm that income is taxed individually. There is no need to register for an Income tax account, you are automatically registered upon submitting a return for the first time.

Register using the relevant section of the business taxes registration application. Corporations must register for either the corporation business tax or business entity tax but not both. Generally C Corporations file corporation business tax while S Corporations file business entity tax.

Register using the relevant section of the business taxes registration application.

Delaware

Delaware

Corporation

Not required

There is no corporate income tax specific registration, but most entities will need to file a combined registration application. There is no registration for the department of state administered franchise tax.

More information: Delaware Department of Finance - Division of Revenue

LLC

Not required

Most LLC types do not file Corporate Income Tax returns. There is no registration for the department of state administered franchise tax.

More information: Delaware Department of Finance - Division of Revenue

Register using the FR-500 application or online system.

Florida

Florida

Corporation

Not required

There is no need to register for a Business Income tax account.

More information: Florida Department of Revenue

LLC

Not required

Some LLCs will need to file a partnership information return. There is no registration required before making this filing.

More information: Florida Department of Revenue

Georgia

Georgia

Corporation

Not required

No separate registration is required for corporate income or net worth tax, but entities may need to register before filing for other taxes.

More information: Georgia Department of Revenue

LLC

Not required

LLCs will typically file partnership income tax, but this depends of how the IRS classifies them. There is no separate registration required for partnership income tax.

More information: Georgia Department of Revenue

Hawaii

Hawaii

Corporation

Not required

There is no separate registration for corporate income tax or franchise tax, but entities will need to register for a tax ID before filing a return. Only banks and financial institutions are required to file franchise taxes.

More information: Hawaii Department of Taxation

LLC

Not required

There is no separate registration for partnership income tax, but entities will need to register for a tax ID before filing a return.

More information: Hawaii Department of Taxation

Idaho

Idaho

Corporation

Not required

Entities are not subject to both franchise tax and corporate income tax. There is no separate registration required for corporate income or franchise tax.

More information: Idaho State Tax Commission

LLC

Not required

LLCs will typically file partnership income tax, but this depends of how the IRS classifies them. There is no separate registration required for partnership income tax.

More information: Idaho State Tax Commission

Illinois

Illinois

Corporation

Not required

There is no separate registration required for business income tax, but firms should use the business registration application to register with the department.

More information: Illinois Department of Revenue

LLC

Not required

LLCs will typically file a partnership income tax return, but this depends of how the IRS classifies them. There is no separate registration required for business income tax, but firms should use the business registration application to register with the department.

More information: Illinois Department of Revenue

Indiana

Indiana

Corporation

Not required

No separate registration is required for corporate income tax, but entities may need to register before filing for other taxes.

More information: Indiana Department of Revenue

LLC

Not required

LLCs will typically file partnership income tax, but this depends of how the IRS classifies them. There is no separate registration required for partnership income tax.

More information: Indiana Department of Revenue

Iowa

Iowa

Corporation

Not required

There is no need to register for a Business Income tax account.

More information: Iowa Department of Revenue

LLC

Not required

LLCs will typically file partnership income tax, but this depends of how the IRS classifies them. There is no separate registration required for partnership income tax.

Register using form CR-16 and completing the required sections. LLCs will typically file partnership income tax, but this depends of how the IRS classifies them.

LLCs may be required to file a partnership return and should register through the online system.

Maine

Maine

Corporation

Not required

There is no need to register before filing corporate income tax. Other tax types may require registration.

More information: Maine Revenue Services

LLC

Not required

There is no need to register before filing corporate income tax. Other tax types may require registration.

More information: Maine Revenue Services

Maryland

Maryland

Corporation

Not required

There is no need to register before filing corporate income tax. Other tax types may require registration.

More information: Comptroller of Maryland

LLC

Not required

There is no need to register before filing corporate income tax. Other tax types may require registration. LLCs may be required to file a pass through entity return.

More information: Comptroller of Maryland

Massachusetts

Massachusetts

Corporation

Not required

There is no separate registration for corporate excise tax, but corporations may need to register for other taxes.

More information: Massachusetts Department of Revenue

LLC

Not required

Most LLC types do not file Corporate Excise Tax returns.

More information: Massachusetts Department of Revenue

Corporations must register before filing corporate franchise tax returns.

LLC

Not required

Most LLC types do not file Corporate Franchise Tax returns, but this depends on their IRS classification. LLCs may also be required to pay the Minimum Fee. If either of these taxes apply, the LLC will need to register.

Corporations must register before filing corporate income and franchise tax returns.

LLC

Not required

Most LLC types do not file Corporate Income or Franchise Tax returns, but this depends on their IRS classification. If either of these taxes apply, the LLC will need to register.

More information: Mississippi Department of Revenue

Corporations must register before filing corporate income and franchise tax returns.

LLC

Not required

Most LLC types do not file Corporate Income, Franchise Tax, or Partnership Tax returns, but this depends on their IRS classification. If any of these taxes apply, the LLC will need to register.

More information: Missouri Department of Revenue

Montana

Montana

Corporation

Not required

There is no need to register before filing corporate income tax. Other tax types may require registration.

More information: Montana Department of Revenue

LLC

Not required

Most LLC types do not file Corporate Income Tax returns.

Corporations must register before filing corporate income tax returns.

LLC

Not required

Most LLC types do not file Corporate Income, Franchise Tax, or Partnership Tax returns, but this depends on their IRS classification. If any of these taxes apply, the LLC will need to register.

More information: Nebraska Department of Revenue

Nevada

Nevada

Corporation

Not required

Entities that file with the Secretary of State are automatically registered for commerce taxes.

More information: Nevada Department of Taxation

LLC

Not required

Entities that file with the Secretary of State are automatically registered for commerce taxes. LLCs are liable to pay commerce tax.

More information: Nevada Department of Taxation

New Hampshire

New Hampshire

Corporation

Not required

There is no need to register for a Business Income tax account, this happens automatically upon filing the first return. Business entities are generally required to file both Business Entity Taxes and Business Profit Taxes.

More information: New Hampshire Department of Revenue Administration

LLC

Not required

There is no need to register for a Business Income tax account, this happens automatically upon filing the first return. Business entities are generally required to file both Business Entity Taxes and Business Profit Taxes.

More information: New Hampshire Department of Revenue Administration

New Jersey

New Jersey

Corporation

Agency:

New Jersey Department of the Treasury - Division of Taxation

The Commerical Activity Tax applies to most business entities in the state of Ohio. You must register first before filing a return. There is no registration for corporation franchise tax.

$30 registration fee unless the applicant is a nonprofit, foreign retailer, government agency, or only applying for a withholding account or agricultural/farming account.

Notes:

Register before filing. Only public service companies need to file business and occupation taxes.

$30 registration fee unless the applicant is a nonprofit, foreign retailer, government agency, or only applying for a withholding account or agricultural/farming account.

Notes:

LLCs may need to file depending on their IRS classification.

LLCs may need to file depending on their IRS classification.

More information: Wisconsin Department of Revenue

Wyoming

Wyoming

Corporation

Not required

Wyoming does not have a corporate income tax.

More information: Wyoming Department of Revenue

LLC

Not required

Wyoming does not have a corporate income tax.

More information: Wyoming Department of Revenue

Filing Fees

Filing fees depend on your individual situation. We do our best to calculate your filing fees

upfront and collect those fees today so we can get started. Your specialist will determine your

exact filing fees and invoice additional fees if required.

When processing government applications or disbursing filing fees, we may add an order processing fee to cover our administrative expenses.